.png)

Page Industries: Trusting the Jockey

Dear Patrons,

This edition of Investor Compass talks about Page Industries Q4FY23, our views on the company, and the course of action going forward.

Results:

- Page Industries’ revenues in Q4FY23 declined by 13% YoY primarily led by a decline in volumes on account of a weak demand scenario and supply chain disruption due to ARS (Auto Replenishment System) implementation across all the product categories.

- EBITDA margin reduced to 13.9% (down 190 bps sequentially) due to operating deleverage along with normalized discretionary expenses i.e. advertisement expenses.

- The results were sharply below the street’s expectations (PAT miss by 41%) plus moderate narrative for the near term resulted into a sharp correction in stock price (~10%) on 26th May 2023.

- Post the results, the street has also cut earnings to the tune of 12-15% for FY24 and 10-12% for FY25.

Deep dive down the memory lane:

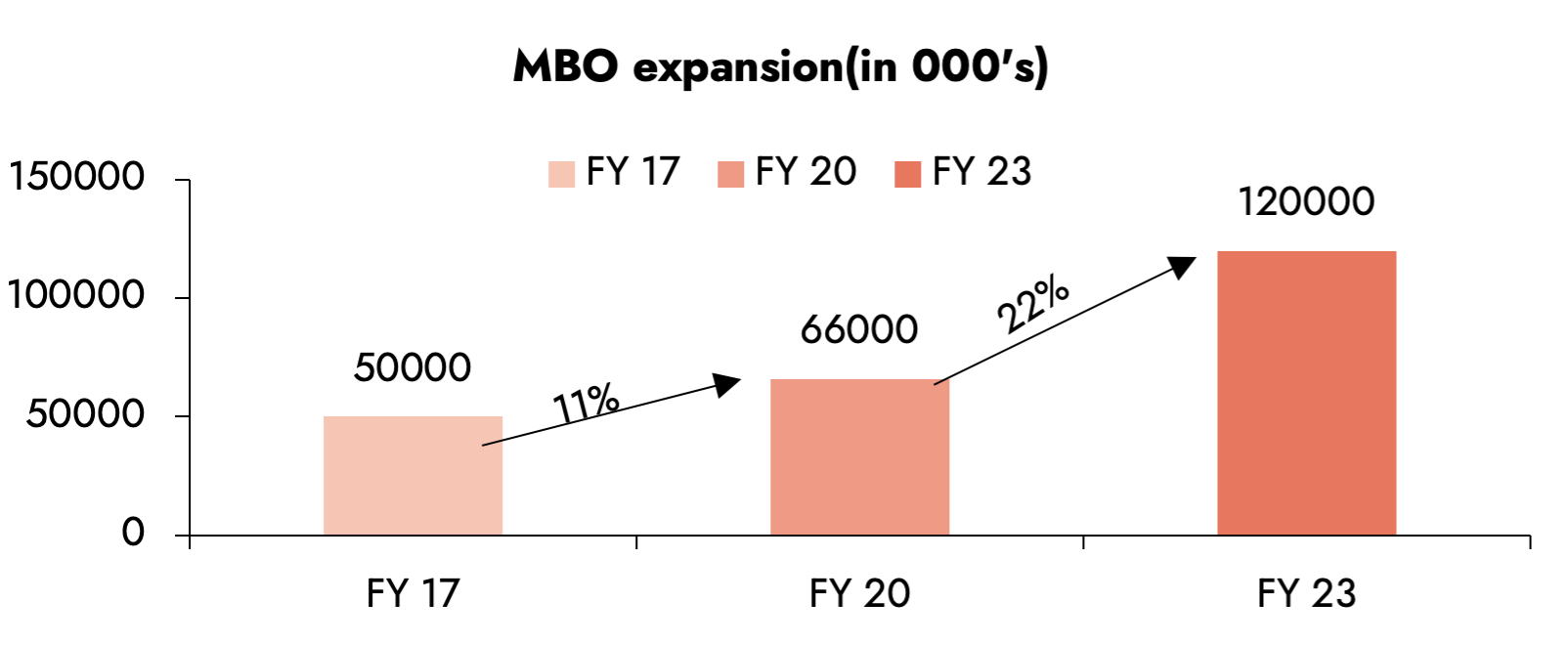

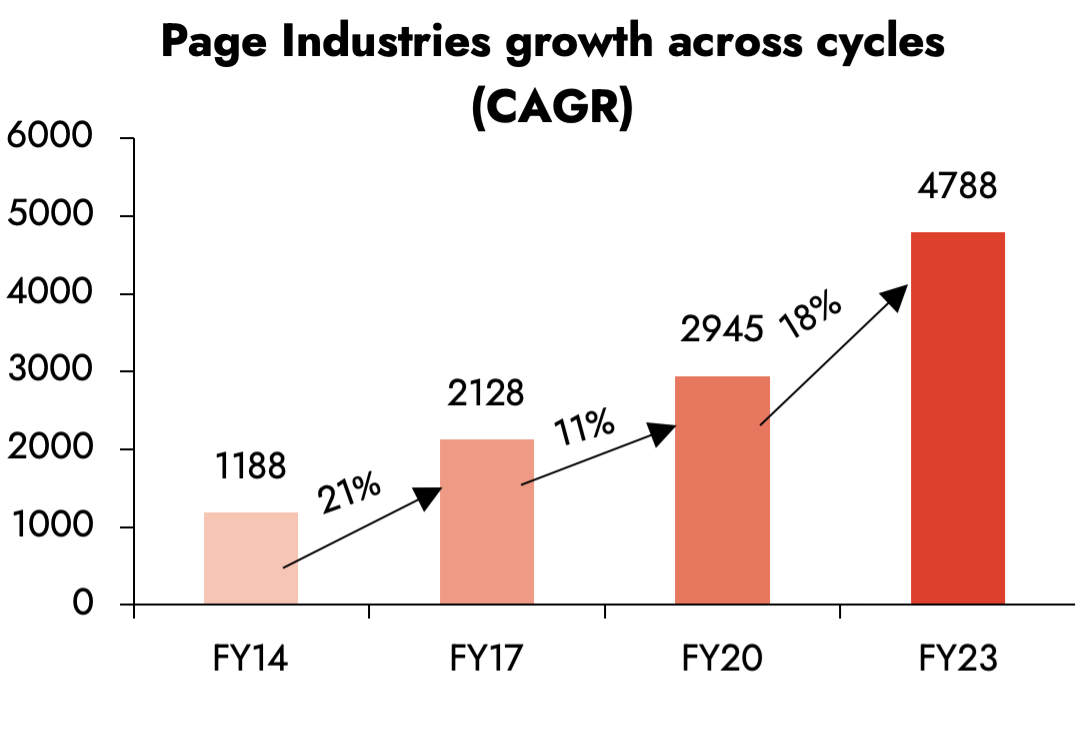

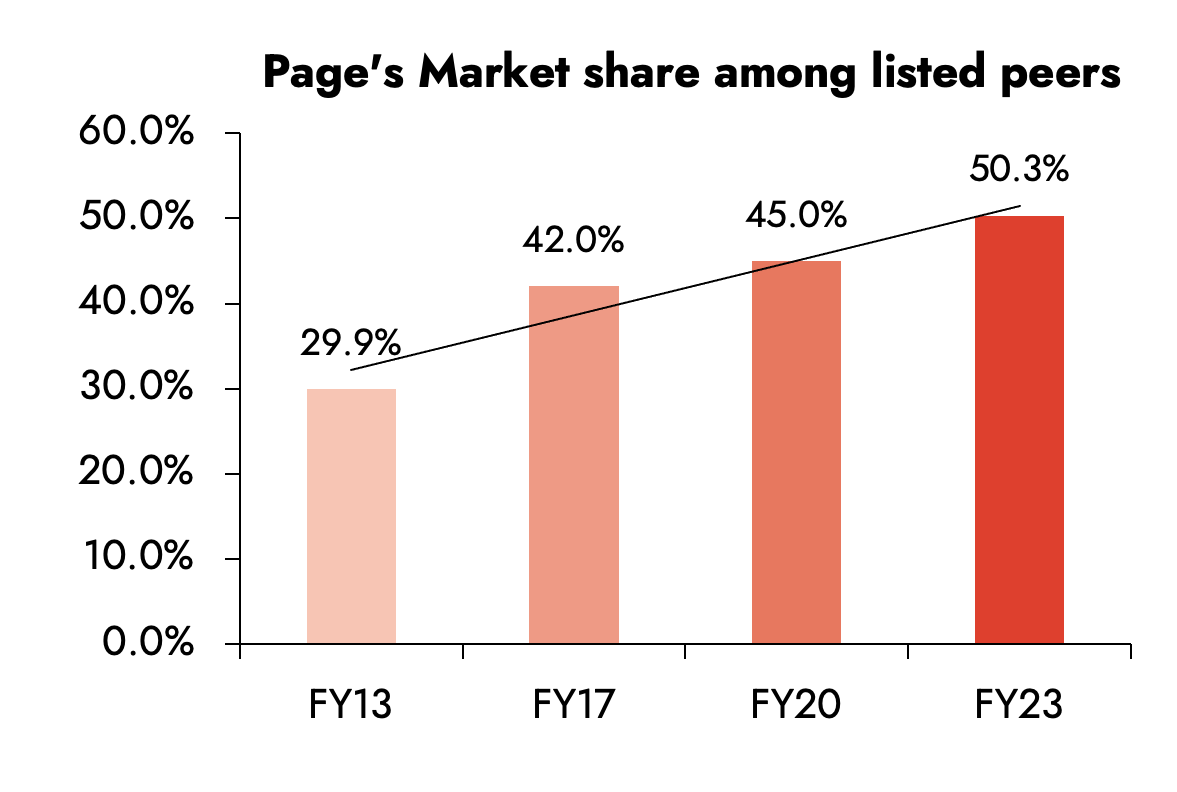

While the street is spooked by the earnings volatility, we believe the concerns are short-sighted. We take precedence of 2017-20 when Page Industries’ growth had been subdued. Page’s growth reduced from ~21% CAGR from FY2014-17 to ~11% in FY2017-20 mainly due to a slowdown at the industry level, discontent among the distributors and rising competitive intensity(Van Heusen).

However, once disruptions subsided, the company grew 18% CAGR over FY20-23, much faster than the industry. Even during the tougher times, Page Industries has managed to garner market share from organized and unorganized players, a testament to the company’s execution.

Source: Ambit Asset management, company

Future Outlook:

- Though the near-term demand trends in the category are muted we anticipate that demand for innerwear will pick up in H2FY24 owing to moderating inflation & consumption picking up.

- ARS – It is a streamlined process that automatically restocks inventory based on predefined criteria at the retail outlet without manual intervention. As per management, the ARS implementation will take another 2 quarters leading to supply chain challenges in the near term, we believe this is a step in the right direction to further strengthen the competitive moats due to:

- Better demand forecasting, optimization of channel inventory & reduction in lead time

- Improvement in working capital resulting into better operating cash flows.

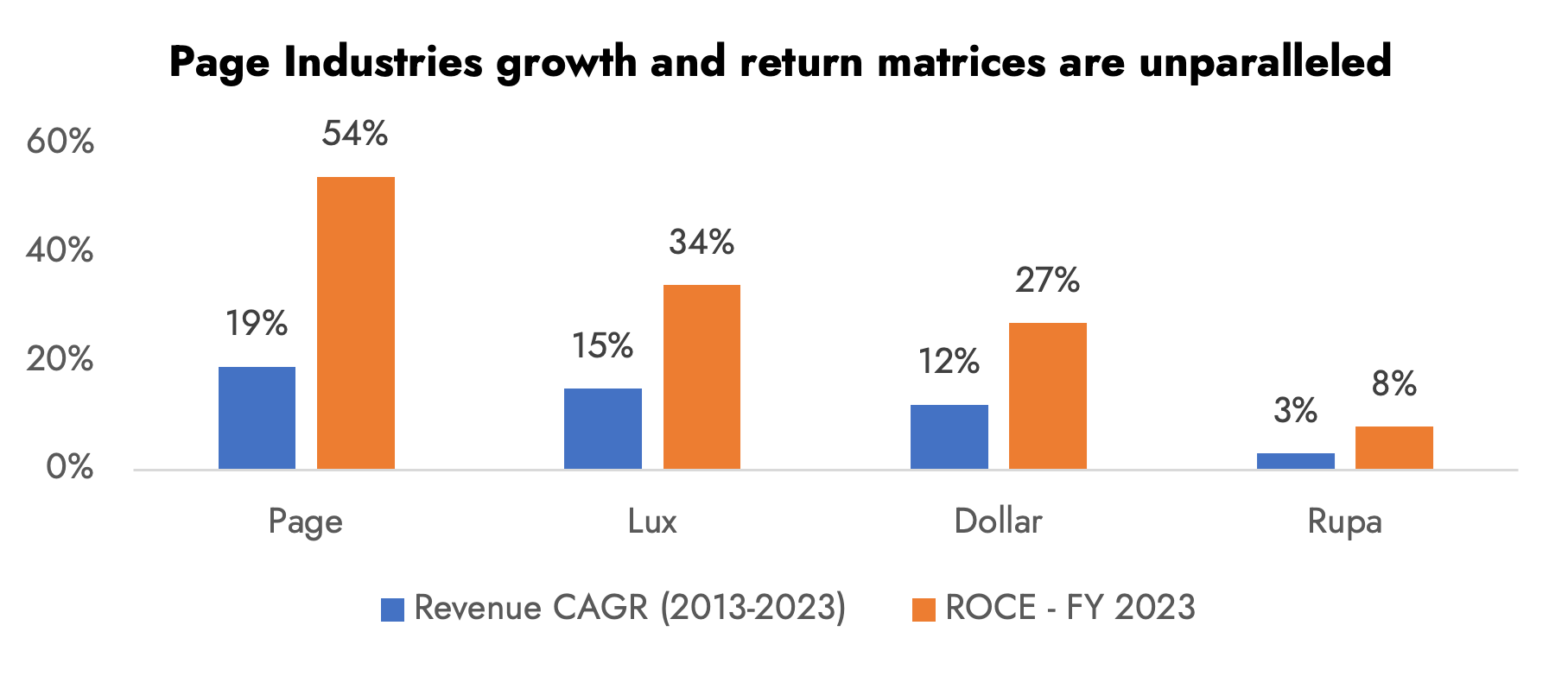

- Page Industries historically has managed to outpace the market by focusing on branding and distribution both in terms of growth and financial matrices.

- The ARS implementation will further strengthen the competitive moats

We believe Page Industries is ideally placed to face the near-term hiccups and come out as a stronger franchise, with lower penetration levels, men’s wear (18%) & other categories (2%-6%). The current short-term pain is temporary in nature and will lead to long-term gains.

For any queries, please contact:

Umang Shah- Phone: +91 22 6623 3281, Email - aiapms@ambit.co. Ambit Investment Advisors Private Limited - Ambit House, 449, Senapati Bapat Marg, Lower Parel, Mumbai - 400 013

Risk Disclosure & Disclaimer

The performance of the Portfolio Manager has not been approved or recommended by SEBI nor SEBI certifies the accuracy or adequacy of the performance related information contained therein.

Ambit Investment Advisors Private Limited (“Ambit”), is a registered Portfolio Manager with Securities and Exchange Board of India vide registration number INP000005059.

This presentation / newsletter / report is strictly for information and illustrative purposes only and should not be considered to be an offer, or solicitation of an offer, to buy or sell any securities or to enter into any Portfolio Management agreements. This presentation / newsletter / report is prepared by Ambit strictly for the specified audience and is not intended for distribution to public and is not to be disseminated or circulated to any other party outside of the intended purpose. This presentation / newsletter / report may contain confidential or proprietary information and no part of this presentation / newsletter / report may be reproduced in any form without its prior written consent to Ambit. All opinions, figures, charts/graphs, estimates and data included in this presentation / newsletter / report is subject to change without notice. This document is not for public distribution and if you receive a copy of this presentation / newsletter / report and you are not the intended recipient, you should destroy this immediately. Any dissemination, copying or circulation of this communication in any form is strictly prohibited. This material should not be circulated in countries where restrictions exist on soliciting business from potential clients residing in such countries. Recipients of this material should inform themselves about and observe any such restrictions. Recipients shall be solely liable for any liability incurred by them in this regard and will indemnify Ambit for any liability it may incur in this respect.

Neither Ambit nor any of their respective affiliates or representatives make any express or implied representation or warranty as to the adequacy or accuracy of the statistical data or factual statement concerning India or its economy or make any representation as to the accuracy, completeness, reasonableness or sufficiency of any of the information contained in the presentation / newsletter / report herein, or in the case of projections, as to their attainability or the accuracy or completeness of the assumptions from which they are derived, and it is expected each prospective investor will pursue its own independent due diligence. In preparing this presentation / newsletter / report, Ambit has relied upon and assumed, without independent verification, the accuracy and completeness of information available from public sources. Accordingly, neither Ambit nor any of its affiliates, shareholders, directors, employees, agents or advisors shall be liable for any loss or damage (direct or indirect) suffered as a result of reliance upon any statements contained in, or any omission from this presentation / newsletter / report and any such liability is expressly disclaimed. Further, the information contained in this presentation / newsletter / report has not been verified by SEBI.

You are expected to take into consideration all the risk factors including financial conditions, risk-return profile, tax consequences, etc. You understand that the past performance or name of the portfolio or any similar product do not in any manner indicate surety of performance of such product or portfolio in future. You further understand that all such products are subject to various market risks, settlement risks, economical risks, political risks, business risks, and financial risks etc. and there is no assurance or guarantee that the objectives of any of the strategies of such product or portfolio will be achieved. You are expected to thoroughly go through the terms of the arrangements / agreements and understand in detail the risk-return profile of any security or product of Ambit or any other service provider before making any investment. You should also take professional / legal /tax advice before making any decision of investing or disinvesting. The investment relating to any products of Ambit may not be suited to all categories of investors. Ambit or Ambit associates may have financial or other business interests that may adversely affect the objectivity of the views contained in this presentation / newsletter / report.

Ambit does not guarantee the future performance or any level of performance relating to any products of Ambit or any other third party service provider. Investment in any product including mutual fund or in the product of third party service provider does not provide any assurance or guarantee that the objectives of the product are specifically achieved. Ambit shall not be liable for any losses that you may suffer on account of any investment or disinvestment decision based on the communication or information or recommendation received from Ambit on any product. Further Ambit shall not be liable for any loss which may have arisen by wrong or misleading instructions given by you whether orally or in writing. The name of the product does not in any manner indicate their prospects or return.

The product ‘Ambit Coffee Can Portfolio’ has been migrated from Ambit Capital Private Limited to Ambit Investments Advisors Private Limited. Hence some of the information in this presentation may belong to the period when this product was managed by Ambit Capital Private Limited.

You may contact your Relationship Manager for any queries.

The performance data for coffee can product between 6th march 2017 - 19th June 2017 represents model portfolio returns. First client was onboarded on 20th June 2017. The performance data for G&C product between 1st June 2016 to 1st April 2018 also includes returns for funds managed for an advisory offshore client. Returns are calculated using TWRR method as prescribed under revised SEBI (Portfolio Managers) Regulations, 2020